Energy access and financial inclusion: Are solar PAYG products promoting digital financial access and use among rural households in Kenya? A case study of Kakamega County

Energy access and financial inclusion: Are solar PAYG products promoting digital financial access and use among rural households in Kenya? A case study of Kakamega County

Beryl Ajwang’, MEM1

Abstract

This study evaluates the impact of adoption of Pay-As-You-Go (PAYG) solar products on digital financial access and use among rural households in Kenya. The study was conducted in Kakamega County with 94% of its population considered off-grid and 85% considered rural. A total of 570 households were interviewed and through the use of statistical analysis, including regression analysis and t-tests, the results were analyzed. Findings from the analysis indicate that there is no significant difference in digital finance access and use between households that have adopted PAYG solar products and those that have not. However, households with PAYG products have a higher frequency and level of use of their mobile wallets as compared to households without. The increased frequency and their repayment history increases their eligibility for credit through their mobile accounts. Informal financial groups have a strong impact on the adoption of PAYG solar products as they help in pooling of risks and reducing the marketing costs involved in the sales of these products. Companies, such Green Planet, are leveraging the existing farmer groups run by One-Acre Fund (a social enterprise that work with farmers to provide seeds and fertilizers on credit in the County) to sell their products. PAYG as a business model has the potential to provide financial services to the unbanked if they are able to carefully assess the lending risks involved. However, to remain sustainable they may have to overcome challenges of a shrinking market size due to parallel government electrification programs and uncertainty in policies regarding mobile money transactions.

Utafiti huu unaangazia athari ya matumizi ya taa za sola ambazo hununuliwa kwa njia ya malipo ya polepole kwenye ufikiaji na matumizi ya fedha za simu vijijini, nchini Kenya. Utafiti huu ulifanyika katika kata ya Kakamega nchini Kenya. Asilimia tisini na nne (94%) ya wakazi wake walichukuliwa kutokuwa na umeme nyumbani na asilimia themanini na tano (85%) walichuliwa kuishi vijijini. Jumla ya nyumba 570 zilitembelewa na wenyeji kuhojiwa. Majibu yalichambuliwa kutumia uchambuzi wa takwimu ikiwa pamoja na regression* na t-test. Matokeo ya uchambuzi yanaonyesha kwamba hakuna tofauti kubwa katika ufikiaji na matumizi ya fedha za simu kati ya nyumba ambazo zinatumia taa za sola za malipo ya polepole na zisizo. Hata hivyo, nyumba zilizo na taa za sola za malipo ya polepole zina kiwango cha juu ya matumizi ya fedha za simu ikilinganishwa na nyumba zisizo. Ongezeko la matumizi ya fedha za simu pamoja na historia yao ya malipo huongeza kiwango cha mikopo kupitia akaunti zao za simu. Zaidi, makundi ya kifedha yasiyo rasmi yanaathiri sana ununuzi na matumizi ya taa za sola za malipo ya polepole kwa kuwasaidia kuunganisha hatari ilhali wakikupunguza gharama za uuzaji zinazohusika katika mauzo ya bidhaa hizi. Makampuni, kama vile Green Planet, wanatumia vikundi vilivyopo vya wakulima vinavyoendesha na shirika la One-Acre Fund (ambayo hufanya kazi na wakulima kutoa mbegu na mbolea kwa mkopo katika Kata) ili kuuza bidhaa zao. Ni wazi kwamba makampuni yanayoendesha malipo ya polepole kama mtindo wa biashara yana uwezekano wa kutoa huduma za kifedha kwa wasio na benki iwapo wanaweza kuchunguza kwa makini hatari za mikopo zinazohusika. Hata hivyo, kubaki endelevu lazima makampuni haya yakabiliana na changamoto za soko kupungua kutokana na mipango sambamba ya serikali kusambaza umeme na kutokuwa na uhakika katika sera zinazohusiana na shughuli za fedha za simu.*

Introduction

Lighting remains one of the leading expenses for households without access to electricity. Globally, it is estimated that households spend 25–30% of their family income on kerosene for lighting and cooking, about US$ 36 billion a year (Pode 2013). In Africa, up to US$ 17 billion is spent on fuel-based lighting sources, with poor households spending 10–15% of their incomes on lighting alone (Lighting Africa 2012). In Kenya, close to 4 million households use kerosene for lighting and spend US$ 2–4 (KES 200–400) per month on kerosene (Lay, 2012) and a total of US$ 157 per year in meeting their energy needs (Bloomberg New Energy Finance 2016).

The massive growth in the solar sector in Kenya has been driven by low electrification rates and the high upfront cost of connection. Considered one of the most mature markets in East Africa, the solar market dates back to the 1980s. The initial solar Photovoltaic (PV) market was dominated by donors such as the World Bank and GEF, who were more interested in the larger applications of PV in schools and communication and did not target households. This disparity resulted in the rise of the private sector, which did eventually steer the market to its present status (Acker 1996). As of 2011, about 320,000 solar home systems had been sold with annual sales of between 20,000–25,000 systems (Lay 2012), bringing the current estimates to a total of 450,000–500,000 installations.

The need to overcome the high upfront cost of solar technologies for modern lighting has seen the emergence of innovative consumer financing models such as the Pay-As-You-Go (PAYG) which operates by extending a credit in form of the solar products to the household and allowing them to pay back over a given period of time. PAYG solar products are replacing kerosene lamps among rural poor households by providing cleaner lighting solutions. Turman-Bryant et al. (2015) posit that PAYG solar products are also promoting digital finance access through the use of mobile wallets among the rural unbanked households. Moreover, they argue that because the asset loans provided through PAYG are of smaller size than was previously possible by formal financial institutions, even low-income households can be reached.

Digital financial access has great benefits to households by allowing them to make and receive payments and access credit without having bank accounts. Further, it increases the incentives to save through default options (World Bank 2016). Studies such as Beck et al. (2007) indicate that the availability of capital allows poor households to realize small business opportunities, which leads to an increase in income, enables them to better absorb shocks such as health issues, allows for household investments in durable goods, home improvements or school fees, and also reduces income inequality.

The use of technology and innovative business models has been considered as a ways to increase financial usage among poor households (World Bank 2014). The PAYG business model leverages the success of mobile money in the country by creating flexibility in payments that favor poor households. This goes above the traditional forms of consumer financing by minimizing transaction costs and accommodating irregular and low incomes.

While previous studies have evaluated the impacts of mobile technology on financial inclusion (Andianaivo 2012, Lundqvist 2014, Olela 2016), this study hopes to contribute to the growing knowledge of how the PAYG business model influences energy access by evaluating the impact of the adoption of PAYG solar products on digital finance access and use among low-income rural households in Kenya. The objectives of the study were to determine (i) the occurrence and use of PAYG solar products in off-grid households, (ii) the factors that determine the adoption of PAYG solar products, and (iii) extent of digital finance usage (e.g., for savings, credits, payments, remittances) among these households.

Methods

Understanding PAYG

Based on the definition by the Global Off-Grid Lighting Association (GOGLA & BNEF 2016) PAYG refers to a variety of technologies, payment rules, ownership and financing structures that allow the end user to pay for solar kits in affordable installments and incorporates a technology enabled mechanism to disable the system if a payment is due. The PAYG products range from the Pico products of less than 10W to solar home systems of about 350W.

The PAYG business model has a growing presence in countries with low electrification rates such as those in Sub-Saharan Africa, and particularly in East Africa. Its success in the region can be attributed to the large presence of off-grid solar products and large off-grid population. Some of the PAYG companies/operators using the PAYG mode in Kenya include; Azuri, Mobisol, M-KOPA, Green Planet, Mibawa, Angaza Design, Divi Power, and BBOxx (GOGLA and BNEF 2016). M-KOPA is the leading PAYG provider with over 500,000 homes connected (M-KOPA 2017)

Study site

Kakamega County is located in western Kenya, with a total population of 1,660,651, according the 2009 census (Commission on Revenue Allocation 2013). The main economic activity of the county is agriculture, with the sector employing 756,711 people while only 2,554 people are on wage employment, according to the 2009 census. About 15% of the population is considered urban with the rest residing in rural areas (Kakamega County Government 2013). In terms of energy access, a great percentage of the population still remains unelectrified with only 5.5% using electricity for lighting. Twenty-eight percent of the households use lanterns (paraffin) for lighting and 63.9% tin lamps indicating that about 95% of the population is dependent on kerosene as the main lighting fuel (Kenya National Bureau of Statistics [NBS] 2013)

The poverty incidence in the County is estimated at 49.2%, slightly above the estimated national level of 45.2% (Kenya NBS 2013). About half the population (809,500) live below the poverty line with a poverty gap of 12%, almost equivalent to the national value of 12.6%. The County is considered the leading contributor to the national poverty rate by a factor of 4.8%. The mean monthly expenditure in the county is US$ 52.30 (KES 5,230; 1 US$ = 100 KES) as compared to the national average of US$ 66.20 (KES 6,620).

Household surveys

A total of 570 households out of 325,167 households in Kakamega County were sampled (Figure 1). Respondents were 58% female and 42% male. A clustered random sampling technique was employed to determine the respondents. In this case, the constituencies were identified as sampling blocks. All sublocations within the constituencies were then listed and randomly selected for the survey, using a computer. About 90 sublocations were sampled during the study. Five to six households were randomly selected and interviewed in each sublocation.

Data analysis

To determine if there was significant difference in digital access and use between solar users and non-solar users, and PAYG and Non-PAYG users, I used a two-sample t-test.

To evaluate the factors that affect the adoption of solar products in Kakamega county, I used logistic regression. Households were scored as solar (1) or non-solar (0) as the dependent variable. Average income, literacy, location (household category), gender, education, main source of employment, membership in a non-formal/formal financial group, and ownership of mobile phone were the independent variables.

To establish what factors influence access and use of digital finance, I used multiple linear regression. The dependent variable was a continuum from 0 to 10, based on summing the scores for the following variables: active mobile account (0.5), when it was activated (>5 years: 0.5, >3 years: 0.8, ≤2 years: 1.0), any family member having an active account (0.5), cell phone ownership (0.5), type of phone (basic: 0.5, feature phone: 0.7, smart phone: 1.0), level of use (basic: 0.5, moderate: 1.0, high: 1.5), frequency of use (daily: 1, ≤every two weeks: 0.5, other: 0.3), savings in the mobile account (2), and credit from mobile accounts (2). The independent variables that were considered for the model were lighting source (solar and non-solar), gender (female, male), education (none, primary, secondary, degree/diploma), main source of income (business, agriculture, employment, other), average income (<10K, 10K–40K, 40K–80K, >80K), household head (male, female).

All analysis was done in R and Minitab.

Results

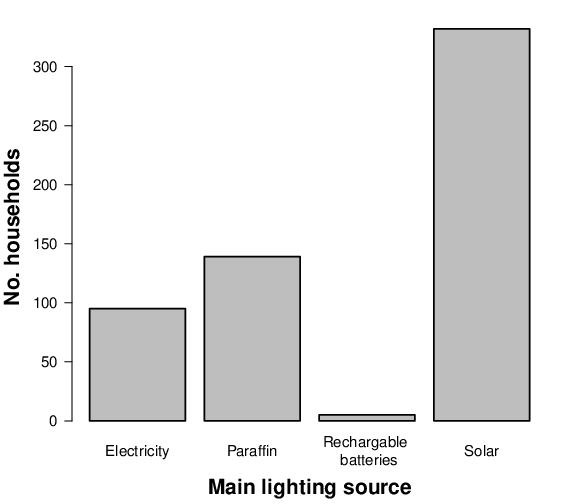

Fifty-eight percent of the sampled population used solar as the main source of lighting with the rest using electricity, paraffin, or rechargeable battery (Figure 2). The solar products used ranged from small solar lanterns to stand-alone solar home systems (PV). Of the 331 households that used solar for lighting, about 61% obtained their products through PAYG processes, in which they made daily or weekly payments.

Households in the Kakamega County still remain largely outside the banking system. Almost half did not have formal bank accounts at all; of those that did, only 36% had active accounts, while the remainder had dormant or deactivated accounts. One of the main reasons stated for lack of accounts was low income. Apart from formal banks, many households were also part of informal financial groups, such as the Village Savings Loan Association (VSLA) and the Rotating and Savings and Credit Association (ROSCA), with only 28% of households not part of any such association. In the past six months, at least 68% of households had deposited savings and 44% taken credit. Credit was mostly taken to cover agricultural purchases (fertilizers and seeds) followed by assets, which in this case were the solar lighting products.

Most households had acquired their solar products via a top-up loan to the basic agricultural loan offered by One-Acre Fund (a social enterprise that works with farmers to provide seeds and fertilizers on credit), which is headquartered in the County.

The mobile penetration rate in Kakamega County was high. A total of 95% of households had a mobile phone and about 76% had activate mobile accounts for at least 5 years whereas only 2.4% had activated their account less than a year ago.

Variation in digital finance use and access

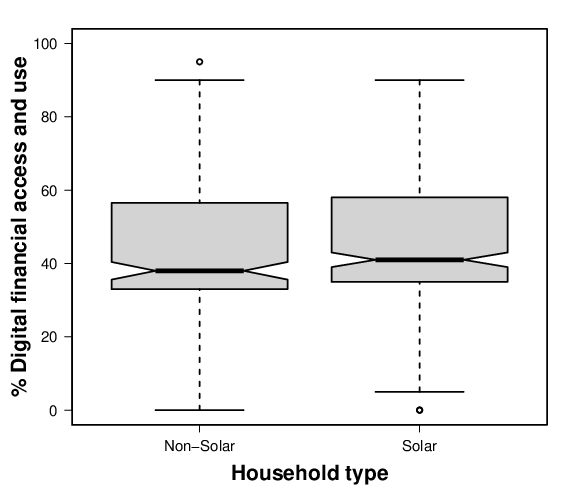

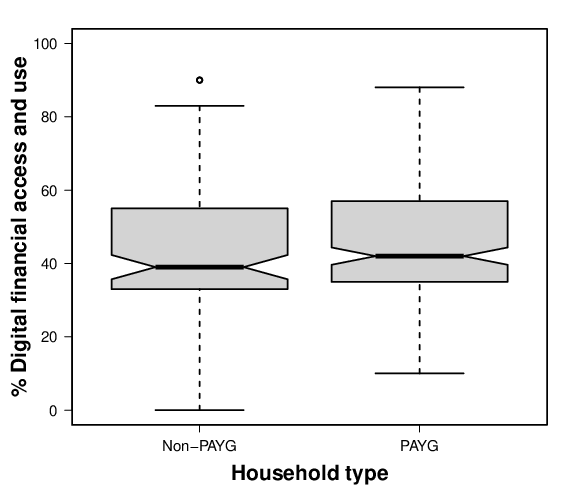

There was minimal variation in digital finance access and use between solar and non-solar house-holds (Figure 3). Similarly, there was no differencein digital finance access and use in solar households between PAYG and non-PAYG (e.g., cash, higher purchase, gift) methods of acquisition (Figure 4).

There was no significant variation in level of access and use of digital finance among the solar and non-solar users (Student’s t-test: t = -1.75, df = 438, P = 0.08) and in the level of use and access of digital financial between households that acquired their solar products through PAYG and Non-PAYG (Student’s t-test: t = -0.79, df = 186, P = 0.43).

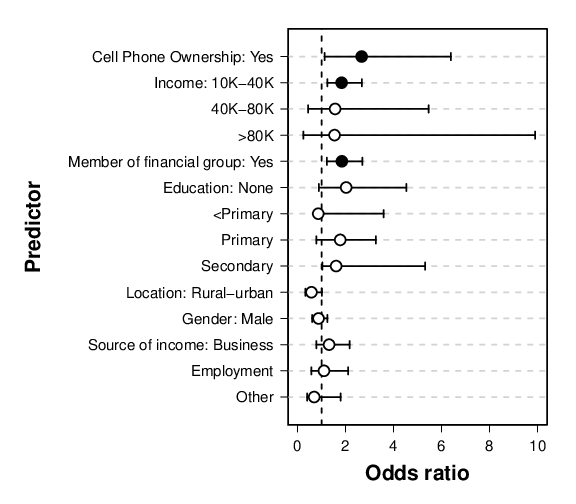

Factors affecting adoption of solar technologies

Possession of a phone, average household income, and membership in a financial group were significant predictors of whether a household adopted solar technology (Figure 5).

Households with cell phones were 2.6 times more likely to use solar products compared to those that did not have cell phones. Additionally, households with low average income had a higher likelihood of taking up solar compared to those with higher income. For example, households with incomes of KES 10,000–40,000 were about 2 times more likely to adopt solar than households with incomes greater than KES 80,000. Households with membership in financial groups—whether formal or non-formal institutions such as village savings—had double the chance of solar adoption.

Factors affecting digital finance access and use

Owning a solar product did not seem to have any significant effect on the access and use of digital finance. Gender, average household income and household main source of income were significant predictors of digital finance access and use among households. Households that had average income levels of KES 10,000-40,000 and those that had business as their main source of income had higher levels of use (Table 1).

| Predictor | Reference Category | Coefficient | P |

|---|---|---|---|

| Household head: | Female | 0.093 | |

| Male | 0.492 | ||

| Av. household income: | 10,000 | 0.022 | |

| 10,000–40,000 | 0.426 | 0.005 | |

| 40,000–80,000 | 0.771 | 0.119 | |

| >80,000 | 0.958 | 0.200 | |

| Education: | Degree/Diploma | 0.058 | |

| None | -0.585 | 0.066 | |

| Less than Primary | -0.172 | 0.637 | |

| Primary | -0.063 | 0.818 | |

| Secondary | 0.126 | 0.653 | |

| Gender: | Female | 0.041 | |

| Male | 0.302 | ||

| Main Source of Income: | Agriculture | 0.001 | |

| Business | 0.718 | 0.000 | |

| Employment | 0.347 | 0.176 | |

| Other | -0.223 | 0.406 | |

| Main lighting source: | Non-Solar | 0.274 | |

| Solar | 0.158 | ||

| Constant | 3.647 | 0.000 |

Discussion and conclusion

Digital financial access and use does not seem to vary between households that acquired their solar products though PAYG and those that acquired them through different means such as cash or higher purchase. However, there seems to be a correlation between the frequency and level of use of mobile money and adoption of PAYG. Households with PAYG have increased rate of use as compared to other households. A possible explanation would be that they have to make weekly or monthly payments. This concurs with the ideas posited by Waldron (2016), that the adoption of PAYG solar products become an activation and increases the use of mobile money. Increased frequency of mobile money use can have direct impacts on access to credit. PAYG companies are also using the repayment history of households to give advanced form of credits such as larger solar panels and smartphones. While this study was focused on a country with a well-established mobile money platform, it would be interesting to see the outcomes for countries that are adopting these solar technologies but do not have elaborate mobile money platform as Kenya.

Households indicated willingness to take up different products on a PAYG model ranging from assets such as water pumps, sewing machines, TV, dairy cows to cash for business and educational purposes. This shows that PAYG companies have the potential of diversifying and ensuring sustainability by moving beyond supplying the regular energy products to offering different products such income generating assets, and loans. MKOPA is already adding TV and clean cooking technologies such as LPG. Given that PAYG companies have established relationships and trust with customers and have existing distribution networks, it becomes easier and cheaper to introduce new products and advance loans based on customer re-payment histories. According to Winicieki (2015) as cited by Waldron and Faz (2016), an accurate assessment of the risk of lending by PAYG solar companies while expanding their markets across the country may set them to become the first scalable model for providing asset financing to unbanked customers.

In order to become sustainable, PAYG companies may have to contend with two main challenges. The first would be parallel programs from the government that target rural-electrification such as the Rural Electrification Program and the Last Mile Connectivity. As demonstrated in their research, Lay, Ondraczek, and Stoever (2013) advance that there is a likelihood that the potential market for solar home systems in off-grid areas would shrink due to grid extension, especially if it is offered at offered on a large scale, predictable and reliable basis. There is also lack of recognition of these products as a means of electrification and hence no direct policy to support this market. There is room for the government to potentially partner with these organizations to offer energy products services to these areas instead of bypassing them. Additionally, as suggested by Lay, Ondraczek, and Stoever (2013) price policies such as subsidies on these products will be beneficial in ensuring the products are competitive enough and affordable to low-income households.

The second challenge would be policy uncertainty in relation to mobile currency regulation and taxes on solar products are at the center of the PAYG business model. Changes in the transaction costs, such as increased exercise duty, have direct impacts on the pricing of products which in turn impacts the purchases and the market size for these companies. In order to address this, the government should ensure that all stakeholders are involved in decision-making for a fair bargain.

Membership in financial groups—whether formal or non-formal institutions such as village savings—seems to be pivotal in the adoption of solar products with households that in groups being twice as likely to adopt than those not in any group. Groups are increasingly becoming a marketing/distribution model for most products that target households at the base of the pyramid-whether asset or fiscal. MFIs and PAYG operators are using agents who in the end target groups to reduce the marketing costs and pool risks. The groups provide a financial guarantee that may not be possible with one person and also reduces the default risk. As was observed in Kakamega County, Green Planet Company, which sells the Sun King products is leveraging existing farmer groups run by One-Acre Fund to sell their products.

Acknowledgements

This work would not have been possible without the financial support of the Yale Tropical Resources Institute. I want to thank Dr. Kenneth Gillingham for his continued support throughout this research, Dr. Oswald Schmitz for his invaluable inputs in shaping my research idea, and Dr. Jonathan Reuning-Scherer for his statistical advice.

My sincere gratitude to fellow students for their genuine critique and unending support throughout this project. A special thank you to Ms. Swetha Kolluri and Ms. Page Weber. I also want to thank the efficient team of enumerators who worked tirelessly with me to ensure that the household data collection was within schedule.

References

Acker, R.H. & Kammen, D.M. 1996. The quiet (energy) revolution: Analysing the dissemination of photovoltaic power systems in Kenya. Energy Policy 24, 81–111.

Ajay, S. & Milca, M. 2014. Sampling techniques and determination of sample sizes in applied statistics research: An overview. International Journal of Economics, Commerce and Management 2, 1–22.

Andianaivo, M. & Kpodar, K. 2012. Mobile phones, financial inclusion and growth. Review of Economics and Institutions 3, 1–30.

Arne, J. 2004. Connective Power: Solar electrification and social change in Kenya. University of California, Berkley, Berkeley, CA, USA.

Beck, T., Demirgüç-Kunt, A. & Levine, R. 2007. Finance, inequality and the poor. Journal of Economic Growth 12, 27–49.

Bloomberg New Energy Finance. 2016. Off-Grid Solar Market Trends Report 2016.

Commission on Revenue Allocation. 2013. Kenya County Fact Sheet.

Erik, H.L. 2013. Pico Solar Home Systems for Remote Homes: A new generation of Small PV systems for lighting and communication. International Energy Agency.

Glenn, D.I. 2003. Determining Sample Sizes. Institute of Food and Agricultural Sciences, University of Florida, Gainsville, FL, USA.

Global, Lighting, and Bloomberg New Energy Finance. 2016. Off-grid solar market trends report 2016. Bloomberg New Energy Finance and Lighting Global in cooperation with the Global Off-Grid Lighting Association (GOGLA)

Kakamega County Government. 2013. First Integrated Development Plan 2013–2017.

Kenya National Bureau of Statistics, Financial Sector Deepening Kenya, and Central Bank of Kenya. 2016. FinAccess Household Survey.

Kenya National Bureau of Statistics, and Society for International Development. 2013a. Exploring Kenya’s Inequality: Pulling apart or pulling together?

Kenya National Bureau of Statistics, and Society for International Development. 2013b. Exploring Kenya’s Inequality: Pulling apart or pulling together? Kakamega County.

Kenya Power and Lighting Company. 2014. Annual Report and Financial Statement 2014/2015.

Lay, J., Ondraczek, J. & Stoever, J. 2012. Renewables in the energy transition: Evidence on solar home systems and lighting-fuel choice in Kenya. GIGA Working Papers 198.

Lighting Africa. 2011. The Off-Grid Lighting Lighting Market in Sub-Saharan Africa: Market research synthesis report.

Lighting Africa. 2012. Lighting Africa Market Trends Report 2012. World Bank/IFC.

Lundqvist, M. & Erlandsson, F. 2014. The Diffusion of Mobile Phones and its Impact on Financial Inclusion and Economic Growth in Africa. Masters Thesis. Lund University, Sweden.

M-KOPA. 2017. Breaking records in financing off grid. URL: http://www.m-kopa.com/breaking-records-in-financing-off-grid/.

Morris, E., Winiecki, J., Chowdhary, S. & Cortiglia, K. 2007. Using Microfinance to Expand Energy Services: Summary of findings. Small Enterprise Education and Promotion Network.

Muthiora, B. 2015. Enabling Mobile Money Policies in Kenya: Fostering a digital financial revolution. GSMA.

Olela., O.L. & Nzioki, P.M. 2016. Assessing the effects of M-Shwari on financial inclusion among muhoroni factory sugarcane out-Growers’ Households in Muhoroni Sub-County, Kenya. European Journal of Business and Management 8, 95–104.

Ondraczek, J. 2013. The sun rises in the east (of Africa): A comparison of the development and status of solar energy markets in Kenya and Tanzania. Energy Policy 56, 407–417.

Pode, R. 2013. Financing LED solar home systems in developing countries. Renewable and Sustainable Energy Reviews 25, 596–629.

Rolffs, P., Byrne, R & Ockwell, D. 2012. Financing Sustainable Energy for All: Pay-as-you-go vs. traditional solar finance approaches in Kenya. STEPS Working Paper. STEPS Centre, Brighton, UK.

Turman-Bryant, N., Alstone, P., Gershenson, D., Kammen, D.M. and Jacobson, A. 2015. Off Grid Power and Connectivity: Pay-As-You-Go financing and digital supply chains for Pico Solar. Lighting Global.

Waldron, D. & Faz, X. 2016. Digitally Financed Energy: How off-grid solar providers leverage digital payments and drive financial inclusion. CGAP, Washington, DC, USA.

Winiecki, J., Kumar, K. & Version, P. 2014. Access to Energy via Digital Finance: Overview of models and prospects for innovation. Consultative Group Assist the Poor.

Winiecki, J. 2015. 4 Ways Energy Access Can Propel Financial Inclusion. URL: http://www.cgap.org/blog/four-ways-energy-access-canpropel-financial-inc….

World Bank. 2014. Global Financial Development Report 2014: Financial Inclusion. Washington, DC, USA.

World Bank. 2016. World Development Report 2016: Enabling digital development digital finance, Washington, DC, USA.

Zeriffi, H. 2011. Innovative business models for the scale-up of energy access efforts for the poorest. Current Opinion on Environmental Sustainability 3, 272–278.

-

Beryl is a recent graduate of the Masters in Environmental Management degree at the Yale School of Forestry and Environmental Studies, with a keen interest in energy and the environment. Before joining Yale, she worked as a research analyst with the EED Advisory, a consulting company on energy, climate change, and natural resources in Kenya. During that period, she provided technical assistance to the Ministry of Environment in modeling GHG emissions in the energy sector and the abatement potential of renewable energy including biogas for cooking; provided climate change data and intelligence as inputs to capacity development curriculum on current topics such as INDCs, NAMA and climate finance; conducted household surveys for the development of Turkana county energy master plan as well as managing an online household energy data aggregator based on the mobile phone technology. She holds BSc in Environmental and Bio-systems Engineering from the University of Nairobi, Kenya.↩